Breadcrumb

4.1.020 Investment Policy

University of Central Missouri Policy

|

Policy Name: Investment Policy |

Date Approved: October 26, 2018 |

|

Policy Category: Board of Governors - Finance and Administration |

Date Effective: October 26, 2018 |

|

Policy Number: BOG 4.1.020 |

Date Last Revised: Approved by the Board of Regents on October 17, 1984 |

|

Approval Authority: UCM Board of Governors |

Review Cycle: Annually by the Treasurer |

|

Responsible Department: Office of the President |

|

To provide guidelines under which the investment of the University will be managed, providing the highest investment return with minimum risk while meeting the daily cash flow demands and conforming to the state laws governing the investment of public funds.

This policy applies to all financial assets of the University eligible for investment and which are accounted for in the University’s annual financial audit.

Pooling of Funds

Except for cash in certain restricted and special funds, the University will consolidate cash balances from all funds to maximize investment earnings. Investment income will be allocated to the various funds based on their respective participation and in accordance with generally accepted accounting principles.

External Management of Funds

Investment through an external registered investment advisor, external programs, facilities and professionals operating in a manner consistent with this policy will constitute compliance.

Missouri Revised Statutes Chapter 174 authorizes the Board of Governors to manage the University's investment program. Deposit and investment of state funds must comply with Article IV, Section 15 of the Missouri Constitution and Chapters 30 and 110 of the Revised Statutes of Missouri. Investments of endowment funds must be made in accordance with Missouri Revised Statutes Chapter 402, the Uniform Prudent Management of Institutional Funds Act. The Board of Governors hereby delegates responsibility for the management of the investment program and written procedures for the operation of the investment program to the President of the University. The treasurer and those persons he/she shall designate are assigned the authority to receive and disburse funds of the University.

The primary objectives, in priority order, of investment activities shall be safety, liquidity, and yield:

Safety of principal is the foremost objective of the investment program. Investments shall be undertaken in a manner that seeks to ensure the preservation of capital in the overall portfolio. The objective will be to mitigate credit risk and interest rate risk.

- Credit Risk

Credit risk is the risk that a security or a portfolio will lose some or all of its value due to a real or perceived change in the ability of the issuer to repay its debt. The University will manage risk by:

- Establishing minimum credit ratings for each non-government security type.

- Implementing a credit review and approval process, or hiring an outside registered investment advisor that has such a process.

- Diversifying the portfolio so that potential losses on individual securities will be minimized.

- Interest Rate Risk

Interest rate risk is the risk that the portfolio value will fluctuate due to changes in the general level of interest rates. It is recognized that all fixed-income investments carry some interest rate risk, and that longer maturities have greater volatility than shorter maturities. The University will manage interest rates risk by:

- Maintaining adequate liquidity for short-term cash needs, and by making longer-term investments only with funds that are not needed for current cash flow purposes.

- Establishing maximum individual investment maturity (or duration) and maximum portfolio average maturity (or portfolio duration) limits.

- Structuring the investment portfolio so that securities mature to meet cash requirements for ongoing operations, thereby avoiding the need to sell securities on the open market prior to maturity.

The investment portfolio shall remain sufficiently liquid to meet all operating requirements that may be reasonably anticipated. This is accomplished by structuring the portfolio so that securities mature concurrent with cash needs to meet anticipated demands (static liquidity). Furthermore, since all possible cash demands cannot be anticipated, the portfolio should consist largely of securities with active secondary or resale markets (dynamic liquidity). A portion of the portfolio also may be placed in bank deposits or repurchase agreements that offer same-day liquidity for short-term funds.

The investment portfolio shall be designed with the objective of attaining a market rate of return throughout budgetary and economic cycles, taking into account the investment risk constraints and liquidity needs. The University may establish a performance benchmark to evaluate performance; however, return on investment is of secondary importance compared to the safety and liquidity objectives described above. Investments are limited to securities considered relatively low risk in anticipation of earning a fair return relative to the risk being assumed.

All participants in the investment process shall act responsibly as custodians of the public trust. The standard of prudence to be applied by the personnel of the Investment Division is the “prudent investor” rule, which states, “Investments shall be made with judgment and care, under circumstances then prevailing, which persons of prudence, discretion and intelligence exercise in the management of their own affairs, not for speculation, but for investment, considering the probable safety of their capital as well as the probable income to be derived.”

Officers and employees involved in the investment process shall refrain from personal business activity that could conflict with the proper execution and management of the investment program, or that could impair their ability to make impartial decisions. Employees and investment officials shall disclose any material interests in financial institutions with which they conduct business. They shall further disclose any personal financial/investment positions that could be related to the performance of the investment portfolio. Employees and officers shall refrain from undertaking personal investment transactions with the same individual with which business is conducted on behalf of the University.

A list will be maintained of financial institutions authorized to provide investment transactions. In addition, a list also will be maintained of approved security broker/dealers selected by creditworthiness as determined by the investment officer and approved by the governing body. These may include “primary” dealers or regional dealers that qualify under Securities and Exchange Commission (SEC) Rule 15C3-1 (uniform net capital rule). All financial institutions and broker/dealers who desire to become qualified for investment transactions must supply the following as appropriate:

- Audited financial statements.

- Proof of National Association of Securities Dealers (NASD) certification.

- Proof of state registration.

- Completed broker/dealer questionnaire.

- Certification of having read and understood and agreeing to comply with the University’s investment policy.

An annual review of the financial condition and registration of qualified financial institutions and broker/dealers will be conducted by the investment officer.

The Executive Vice President and Chief Operating Officer is responsible for establishing and maintaining an internal control structure that will be reviewed annually with the University’s independent auditor. The internal control structure shall be designed to ensure that the assets of the University are protected from loss, theft or misuse and to provide reasonable assurance that these objectives are met. The concept of reasonable assurance recognizes that (1) the cost of control should not exceed the benefits likely to be derived and (2) the valuation of costs and benefits require estimates and judgements by management.

The internal controls shall address the following points:

- Control of collusion.

- Separation of transaction authority from accounting and record keeping.

- Custodial safekeeping.

- Avoidance of physical delivery securities.

- Clear delegation of authority to subordinate staff members.

- Written confirmation of transactions for investment and wire transfers.

- Development of a wire transfer agreement with the lead bank and third party custodian.

Securities will be held by an independent third-party safekeeping institution selected by the University. All securities will be evidenced by safekeeping receipts in the University’s name. The safekeeping institution shall annually provide a copy of its most recent report on internal controls – Service Organization Control Reports (formerly 70, or SAS 70) prepared in accordance with the Statement on Standards for Attestation Engagements (SSAE) No., 16 (effective June 15, 2011).

Securities may only be sold prior to maturity for the following reasons:

- To meet unexpected liquidity needs.

- To reduce credit risk or minimize loss of principal.

- As part of a security swap that would improve the quality, yield, or expected return of the portfolio.

- To adjust or rebalance the portfolio to be in compliance with policy guidelines, to better match expected cash flows, to better match the target portfolio duration, or to better match a designated performance benchmark.

Securities sold prior to maturity specifically at the request of the University of Central Missouri to meet unexpected liquidity needs are to be reported to the Board Finance Committee by the Executive Vice President and Chief Operating Officer.

The following security types are authorized for the investment of funds by the University:

- United States Treasury Securities – U.S. Treasury and other government obligations that carry the full faith and credit of the United States for the payment of principal and interest. This includes investment in Treasury bills, notes, bonds, strips, and Treasury inflation protected securities (TIPS).

- United States Agency Securities - Obligations, participations, or other instruments issued or guaranteed by any U.S. government agency, instrumentality, or government sponsored enterprise (GSE). This includes investment in coupon issues, zero coupon issues and strips, discount notes, callable securities, step-up coupons, floating-rate coupons, and mortgage-backed securities.

- Repurchase Agreements – Repurchase agreements between the University and a commercial bank or primary government securities dealer. Investment in repurchase agreements must be covered by a signed master repurchase agreement substantially of the standard form designated by SIFMA. Accepted collateral includes only securities in A and B above, and must be collateralized at a minimum of 102%.

- Collateralized Public Deposits (Certificates of Deposit) - Instruments issued by financial institutions which state that specified sums have been deposited for specific periods of time and at specified rates of interest. The certificates of deposit are required to be backed by acceptable collateral securities as dictated by State statute.

- Bankers’ Acceptances - Bills of exchange or time drafts on and accepted by a commercial bank, otherwise known as bankers’ acceptances. An issuing bank must have received the highest letter and numeral ranking (i.e., A1 / P1) by at least two nationally recognized statistical rating organizations (NRSRO’s). Must be issued by domestic commercial banks. Purchases of bankers’ acceptances may not exceed 180 days to maturity. No more than 5% of the total market value of the portfolio may be invested in the bankers’ acceptances of any one issuer and no more than 25% of the entire portfolio may be invested in banker’s acceptances.

- Commercial Paper - Commercial paper rated A-1, P-1, or the equivalent by at least two nationally recognized statistical rating organizations (NRSRO’s). Eligible paper is further limited to issuing corporations that have a total commercial paper program size in excess of $250,000,000 and have long term debt ratings, if any, of “A” or better from at least one NRSRO. Purchases of commercial paper may not exceed 180 days to maturity.

Additionally, purchases of commercial paper in industry sectors that may from time to time be subject to undue risk and potential illiquidity should be avoided. The only asset-backed commercial paper programs that are eligible for purchase are fully supported programs that provide adequate diversification by asset type (trade receivables, credit card receivables, auto loans, etc.). No securities arbitrage programs or commercial paper issued by Structured Investment Vehicles (SIV’s) shall be considered. No more than 5% of the total market value of the portfolio may be invested in the commercial paper of any one issuer. No more than 25% of the entire investment portfolio may be invested in Commercial Paper. Commercial paper issuers must be subject to weekly credit review and daily news research and analysis and a monitoring program must be established to promulgate best practices credit monitoring.

7. Negotiable Certificates of Deposit – Negotiable certificates of deposit issued by a nationally or state-chartered bank or by a nationally or state-licensed branch of a foreign bank. At the time of purchase, the security must have a short-term rating of A-1, P-1, or the equivalent by at least two nationally recognized statistical rating organizations, or a long term rating of the three highest long term rating categories by at least two nationally recognized statistical rating organizations.

8. Corporate Bonds – Investment grade corporate bonds, rated A- or better by at least two nationally recognized statistical rating organizations (NRSROs).

9. Money Market Mutual Funds – Registered money market mutual funds that adhere to SEC rule 2a-7, and are rated AAA or the equivalent by at least one nationally recognized statistical rating organization.

- U.S. Govt. Agency Coupon and Zero Coupon Securities. Bullet coupon bonds with no embedded options with maturities of five (5) years or less.

- U.S. Govt. Agency Discount Notes. Purchased at a discount with maximum maturities of one (1) year.

- U.S. Govt. Agency Callable Securities. Restricted to securities callable at par only with final maturities of five (5) years or less.

- U.S. Govt. Agency Step-up Securities. The coupon rate is fixed for an initial term. At coupon date, the coupon rate rises to a new higher fixed term. Restricted to securities with final maturities of five (5) years or less.

To provide for the safety and liquidity of the University’s funds, the investment portfolio will be subject to the following restrictions:

- Borrowing for investment purposes (“Leverage”) is prohibited.

- Instruments known as variable rate demand notes, floaters, inverse floaters, leveraged floaters, and equity-linked securities are not permitted. Investment in any instrument, which is commonly considered a “derivative” instrument (e.g. options, futures, swaps, caps, floors, and collars), is prohibited.

- Contracting to sell securities not yet acquired in order to purchase other securities for purpose of speculating on developments or trends in the market is prohibited.

Collateralization will be required on two types of investments: certificates of deposit and repurchase agreements. The market value (including accrued interest) of the collateral should be at least 100%.

For certificates of deposit, the market value of collateral must be at least 100% or greater of the amount of certificates of deposits plus demand deposits with the depository, less the amount, if any, which is insured by the Federal Deposit Insurance Corporation, or the National Credit Unions Share Insurance Fund. All securities, which serve as collateral against the deposits of a depository institution, must be safekept at a non-affiliated custodial facility. Depository institutions pledging collateral against deposits must, in conjunction with the custodial agent, furnish the necessary custodial receipts with five business days from the settlement date.

The University shall have a depository contract and pledge agreement with each safekeeping bank that will comply with the Financial Institutions, Reform, Recovery, and Enforcement Act of 1989 (FIRREA). This will ensure that the University’s security interest in collateral pledged to secure deposits is enforceable against the receiver of a failed financial institution.

These securities for which repurchase agreements will be transacted will be limited to U.S. Treasury and government agency securities that are eligible to be delivered via the Federal Reserve Fedwire book entry system. Securities will be delivered to the University’s designated Custodial Agent. Funds and securities will be transformed on a delivery vs. payment basis.

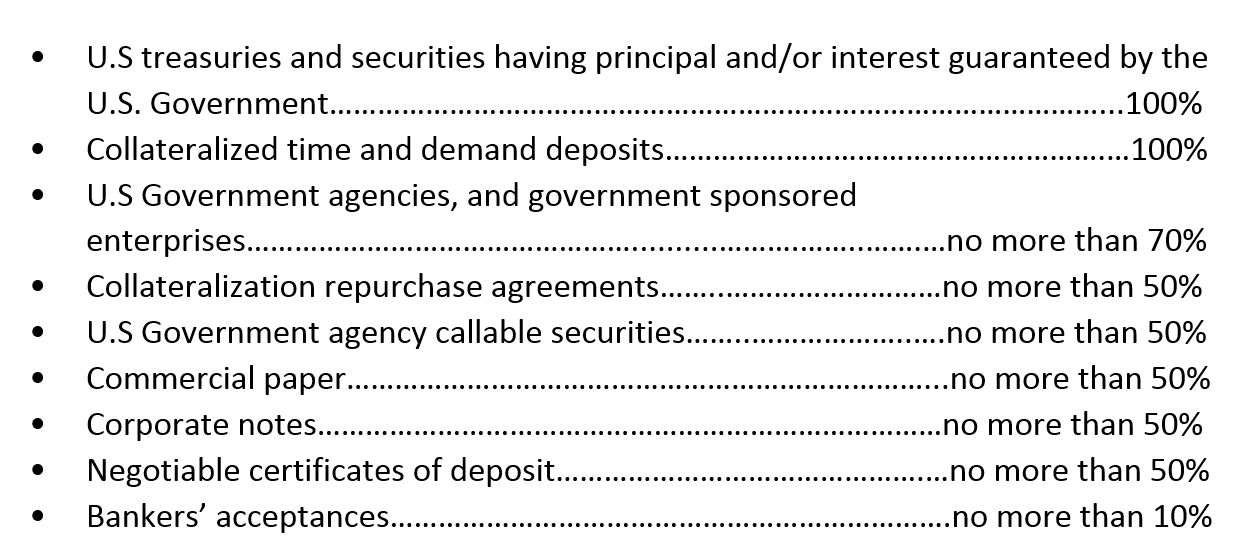

The investments shall be diversified to minimize the risk of loss resulting from over concentration of assets in specific maturity, specific issuer, or specific class of securities. Diversification strategies shall be established and periodically reviewed. At a minimum, diversification standards by security type and issuer shall be:

|

To the extent possible, the University shall attempt to match its investments with anticipated cash flow requirements. No investment shall have a maturity longer than 5 years from the date of settlement. Investments are subject to the following maximum maturities:

|

• U.S. Treasuries |

5 years |

|

• U.S. Government Agencies |

5 years |

|

• Repurchase Agreements |

90 days |

|

• Bankers’ acceptances |

180 days |

|

• Commercial Paper |

270 days |

|

• Corporate Bonds |

5 years |

|

• Negotiable CDs |

5 years |

No more than 5% of the total market value of the portfolio may be invested in any one non-government issuer. Investments in bankers’ acceptances, commercial paper, negotiable CDs, and corporate notes will be combined to determined aggregate exposure.

The treasurer shall prepare an investment report at least quarterly, including a management summary that provides an analysis of the status of the current investment portfolio and transactions made over the last quarter. This management summary will be prepared in a manner that will allow the University to ascertain whether investment activities during the reporting period have conformed to the investment policy. The report should be provided to the Board of Governors of the University. The report will include the following:

- Listing of individual securities held at the end of the reporting period.

- Realized and unrealized gains or losses resulting from appreciation or depreciation by listing the cost and market value of securities over one-year duration (in accordance with Government Accounting Standards Board (GASB) 31 requirements). [Note, this is only required annually]

- Average weighted yield to maturity of portfolio an investments as compared to applicable benchmarks.

- Listing of investment by maturity date.

- Percentage of the total portfolio which each type of investment represents.

The investment portfolio will be managed in accordance with the parameters specified within this policy. The portfolio should obtain a market average rate of return during a market/economic environment of stable interest rates. A series of appropriate benchmarks may be established against which portfolio performance shall be compared on a regular basis.

The market value of the portfolio shall be calculated at least quarterly and a statement of the market value of the portfolio shall be issued at least annually to the governing body of the University. This will ensure that review of the investment portfolio, in terms of value and price volatility, has been performed.

Any investment currently held that does not meet the guidelines of this policy shall be exempt from the requirements of this policy. At maturity or liquidation, such monies shall be reinvested only as provided by this policy.

The Investment Policy shall be reviewed by the University’s Treasurer on an annual basis and any modifications made thereto must be approved by the Board of Governors before becoming effective.